When the Marketplace Becomes the Lender

Jane (Jian) Li , Stefano Pegoraro

Based on: “Borrowing from a Bigtech Platform,” Review of Financial Studies, forthcoming.

Bigtech platforms reshape lending landscape: more get credit but some borrowers suffer.

Share:

The New Lenders on the Block

Traditionally, bigtech platforms have provided value to merchants by enabling them to transact with buyers. When a restaurant signs up with DoorDash or a small retailer joins Amazon’s marketplace, they are gaining access to customers. Increasingly, they are also gaining access to capital. These bigtech platforms — Amazon, PayPal, DoorDash, and Square — now lend billions of dollars directly to the merchants operating on their marketplaces. Globally, bigtech firms lent $572 billion in 2019 — a more than fiftyfold growth since 2013.

These are not ordinary business loans. Platforms typically offer uncollateralized, short-term credit to small and medium enterprises. Furthermore, they collect repayments in an untraditional way: a fixed share of the merchant’s sales on the platform is deducted to repay the loan. This revenue-based repayment mechanism is a key feature of bigtech lending and is closely connected with bigtech platforms’ business. The synergy between lending and their marketplaces gives these bigtech platforms a powerful advantage over traditional banks in lending to small businesses.

Does bigtech lending improve overall credit supply? And does this new form of lending help all borrowers equally, or does it create distributional consequences? Given the unique structure of bigtech lending and its rapid growth, understanding who wins and who loses is a central question for regulators and practitioners alike.

Economy of Scope between Marketplace and Lending

A lot of attention has been devoted to the use of big data and machine learning in fintech lending, but an advantage that the bigtech platform has over traditional banks has been overlooked: the economic value of staying on the platform. The synergy with its marketplace business allows the platform as a lender to better enforce loan repayment compared to traditional banks.

A small merchant who sells through Amazon depends on Amazon for access to hundreds of millions of customers. Leaving the marketplace is not just inconvenient — it is commercially devastating. This dependency gives the platform an enforcement advantage on its loans: because the merchant would lose so much by exiting, the platform can credibly deduct a share of revenue as loan repayment without losing the merchant, effectively enforcing partial repayment even from a merchant who might otherwise default. Absent such dependency on its marketplace, the merchant can easily avoid the repayment fee by operating outside of the platform. In addition, such repayment fees also improve the merchant’s ex-post incentives to repay the loan balances. This enforcement power is stronger for merchants who rely more heavily on the platform for sales, which are typically small businesses that are deemed too risky for traditional banks. For these borrowers, bigtech lending creates a genuine welfare improvement: merchants who would otherwise have no credit at all gain access to capital that lets them invest, grow, and smooth their operations.

A Surprise in the Competitive Segment — Advantageous Screening

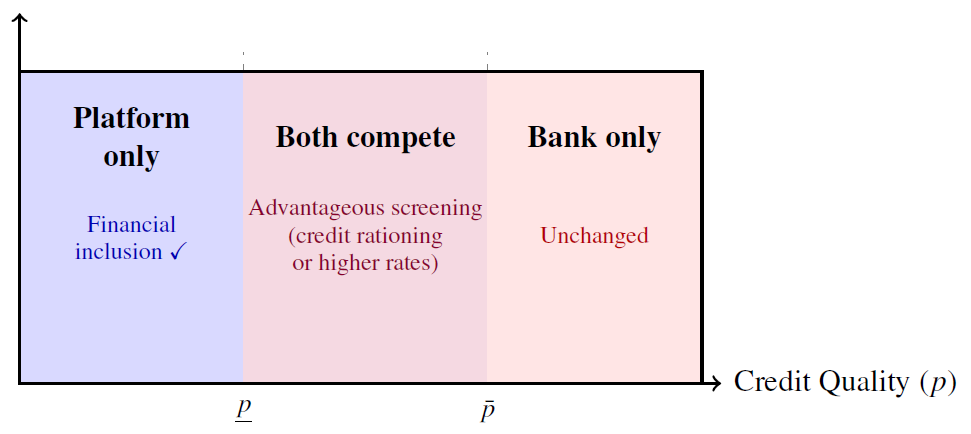

While the bank potentially has lower cost of capital due to its deposit franchise, the platform has an enforcement advantage. The two forces segment the loan market into three groups of borrowers, as shown in Figure 1 below: the safest borrowers are served exclusively by the bank, the riskiest borrowers are served exclusively by the platform, and both lenders compete for the middle segment of borrowers. The story gets more nuanced for this intermediate credit quality segment where the platform and the bank compete for the same set of borrowers.

Figure 1: Credit Market Segmentation

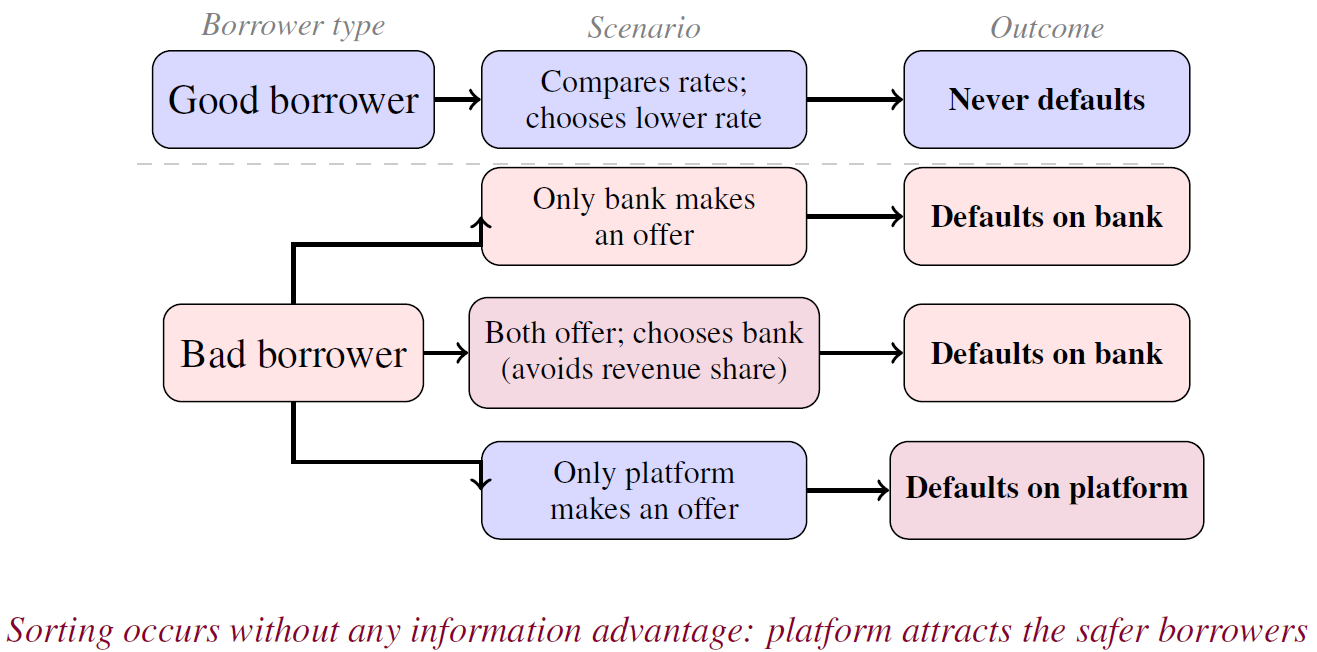

In this competitive segment, the platform gains a second endogenous advantage over the bank from the structure of competition. Consider two merchants with the same public credit profile but have private information about their likelihood of default, perhaps due to the difference in the success rate of their business ventures. Now both are deciding whether to borrow from the bank or from the platform.

The merchant who is more likely to default will always prefer the bank. Because a platform loan comes with revenue-based repayment fees deducted upfront from marketplace sales, a merchant who knows she has high default probability prefers to avoid such a form of contract. In other words, borrowing from the platform is more costly for merchants who are more likely to default. The merchant who intends to repay, by contrast, is largely indifferent to the revenue-based repayment plans — she is likely going to repay anyway. She simply compares the interest rates offered and picks the cheaper option.

As a result, merchants self-sort: those who are more likely to default systematically gravitate toward bank loans, while the platform attracts a disproportionate share of reliable borrowers. The platform benefits from this “advantageous screening,” not because it is smarter or technologically superior, but because its enforcement tool creates a self-selection filter. Figure 2 below illustrates this self-selection mechanism.

Figure 2: The Self-Selection Mechanism

This screening advantage has implications that reverse the usual predictions in credit competition. For example, the platform’s profit may actually rise with the bank — its competitor’s — lending probability. In fact, for certain merchants, the platform is only willing to lend when the bank is present — because a larger bank presence generates more defaulting borrowers self-selecting into bank contracts, boosting the platform’s screening rents. Bank lending and platform lending become complements, not substitutes, even as the two compete directly.

When Banks Pull Back — and Welfare Falls

The bank is not oblivious to what is happening. It observes that the merchants gravitating toward its loans are disproportionately the ones more likely to default. Its rational response is to tighten credit: raise rates, reduce lending probability, or both. In the competitive segment, this may result in credit rationing, even though those merchants will be able to secure credit when the bank is the only lender.

For merchants in this intermediate credit-quality segment where both types of lenders are present, outcomes are worse than in a world with only banks. Credit rationing is more common due to the bank’s response to adverse selection. Furthermore, when credit does arrive, it may come from the platform whose cost of capital exceeds the bank’s, making loans more expensive.

The aggregate welfare picture is therefore mixed. Platform entry unambiguously helps the unbanked — those with weak credit profiles who gain credit for the first time. But for merchants in the competitive segment, platform entry can reduce welfare through higher rationing and higher borrowing costs.

Crucially, this deterioration is not caused by predatory behavior or platform market power in the conventional sense. It is a structural consequence of the platform’s enforcement advantage itself. The very feature that makes bigtech lending inclusive for the unbanked is what drives banks to tighten credit for borrowers in the middle.

What This Means for Regulators

Policymakers around the world have generally welcomed bigtech lending as a force for financial inclusion and competition. Our analysis suggests a closer investigation is warranted.

First, the impact on incumbent bank credit supply matters as much as the direct inclusion benefit. Regulators monitoring only the number of new borrowers reached by bigtech platforms will miss the credit rationing imposed on existing borrowers in the competitive segment. Inclusion metrics alone are insufficient.

Second, credit rationing in the middle of the credit-quality distribution deserves attention. It is precisely the merchants who almost qualify for bank credit — those with intermediate credit scores — who are most at risk from the bank’s adverse-screening response. These are often the small businesses that regulators want to support the most.

Third, the intuition that stronger platform enforcement always improves outcomes does not hold. Greater enforcement power by the platform can intensify the advantageous screening in ways that reduce total lending as banks scale back. Hence, marketplace dynamics and network effects that strengthen platform enforcement may have spillover effects on the loan market, especially on banks’ credit supply.

Ultimately, a more comprehensive approach to bigtech regulation is warranted. Restricting bigtech lending to protect banks could reduce financial inclusion for underserved borrowers. Permitting unrestricted entry may reduce welfare for the middle segment through negative effects on bank credit supply. The optimal policy must weigh both effects, ideally calibrating oversight of the segment of the credit market where displacement is occurring.

The Bottom Line

The prominent role of large bigtech platforms in the modern economy allows them to exploit network effects and economies of scope between their marketplace and lending. Bigtech platforms exploit a genuine and powerful enforcement advantage that helps the unbanked and should be celebrated. But that same advantage reshapes the competitive landscape for banks, inducing them to potentially ration credit more. Getting bigtech regulation right requires recognizing and weighing both effects at the same time.