When Deposits Become a Burden

Patrick Bolton , Ye Li , Neng Wang , Jinqiang Yang

Based on: “Dynamic Banking and the Value of Deposits,” Journal of Finance, 2025, 80(4), 2073–2124.

The curse of abundant deposits: more funding can mean less lending when equity capital is tight.

Share:

In early 2020, as the Covid-19 pandemic hit the global economy, deposits surged on bank balance sheets. JP Morgan Chase saw its deposit base jump 18% in a single quarter. Citigroup and Bank of America experienced double-digit increases. Conventional wisdom says deposits are a bank’s lifeblood—cheap, stable funding. Yet these deposit inflows did not boost bank stock valuations, nor did they stimulate lending. In the meantime, U.S. regulators scrambled to relax the supplementary leverage ratio (SLR) as banks raised concerns over the consequences of this deposit influx.

What are the concerns over abundant deposits? When do deposit inflows turn from a boon to a curse? We develop a dynamic banking model with sticky deposits and costs of external bank equity financing to analyze this question, derive the marginal value of deposits, and draw several new empirically testable predictions. Our analysis highlights a fundamental but underappreciated facet of banking: banks cannot fully control their deposits. When you open a checking account, the bank commits to let you deposit and withdraw freely. This is essential for the payment system—paychecks arrive, rents get paid, and funds move between accounts all day. Unlike bonds or other borrowings that a bank can choose not to roll over at maturity, deposits come and go at the depositor’s discretion. A deposit is, in effect, a perpetual contract between the bank and the depositor, with a stochastic maturity.

The key variable driving the bank’s financial condition is the ratio of a bank’s equity capital to its deposits—call it k. The bank’s inability to control deposits translates into randomness in k. When k is high, the bank is well capitalized and deposits are genuinely valuable: they provide cheap funding that can be channeled into profitable lending, which is in line with the conventional wisdom. But when k is low—when equity is thin relative to deposits—the picture reverses. Additional deposit inflows push k even lower, increase leverage, driving the bank closer to breaching its leverage requirement set by regulators. To stay in compliance, the bank may be forced into a costly equity issuance at that point. The marginal value of deposits—the “deposit q” by analogy with Tobin’s q for physical capital—then turns negative. More deposits mean less shareholder value.

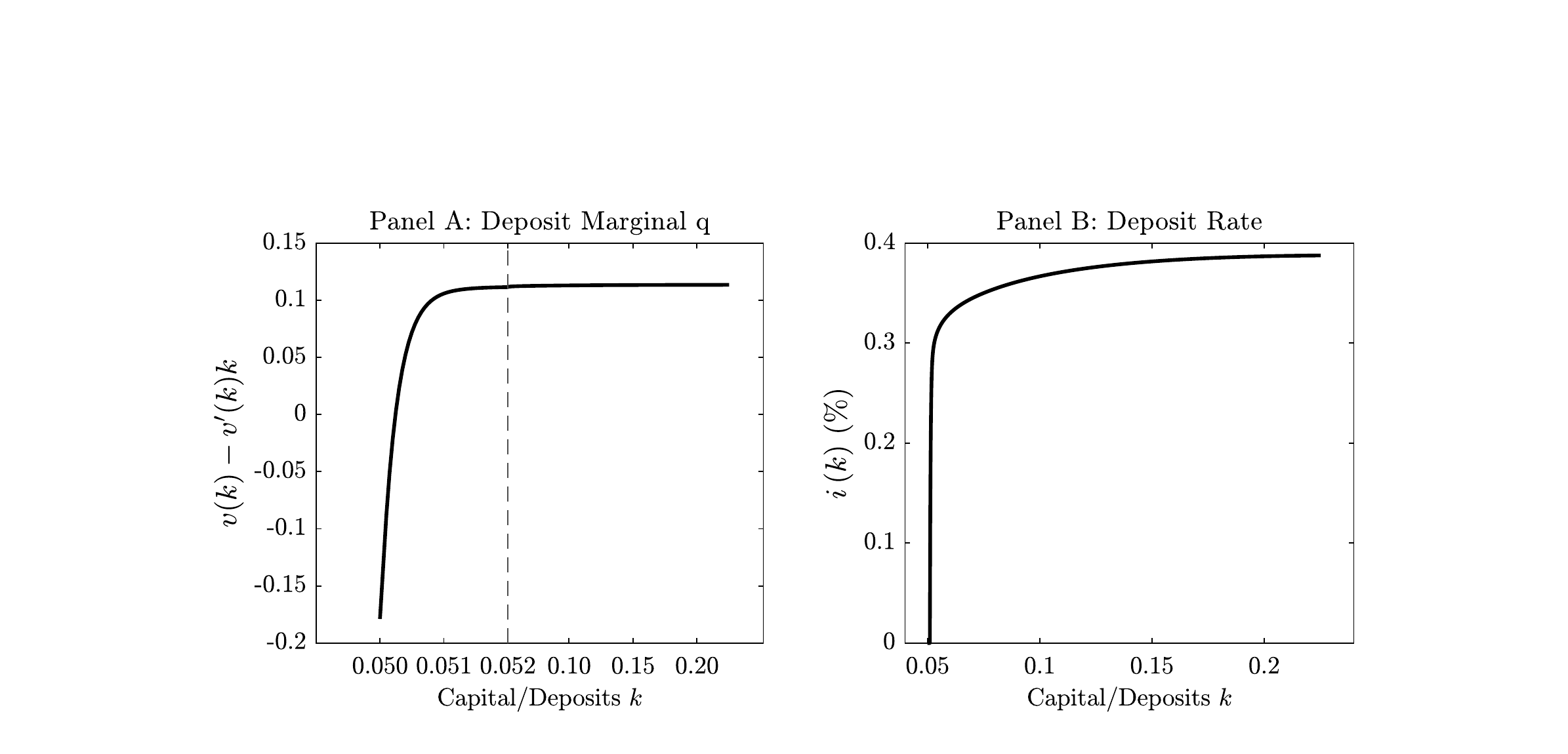

Figure 1. Deposit marginal q and deposit rate.

Figure 1 illustrates an important result of the paper. Panel A shows how the marginal value of deposits swings from positive to deeply negative as the bank’s capitalization deteriorates. In Panel A, the x-axis is stretched near the lower boundary to show the sharp transition. For most of the time, the bank is comfortably capitalized, and one dollar of deposit inflow creates roughly 11 cents for the bank’s shareholders, raising the franchise value from cheap deposit financing. But as k approaches the regulatory boundary, the deposit marginal q plunges to around negative 18 cents. This is a continuous yet sharp decline. Panel B shows how the bank responds when k approaches the regulatory boundary: it slashes the deposit rate to disincentivize inflows. But there is a lower bound for the deposit rate, zero. It is extremely rare that banks charge negative rates on deposits given that cash can always serve as an alternative; so once the rate hits zero, the bank completely loses this instrument for controlling its liabilities and leverage.

The analogy to the q-theory of investment is instructive. For non-financial firms, investment is driven by the ratio between marginal q and marginal value of liquidity—firms invest when this ratio exceeds one, because new productive capital is valuable. For banks, deposits play a role that is analogous to productive capital. Building a deposit base is like building a customer base (or customer capital): the current deposit stock generates ongoing funding-cost advantages, and its effects are persistent because depositors are slow to switch banks. But unlike customer capital, deposits can become liabilities once the bank is close to breaching its leverage requirement. The deposit q can go negative, yet the bank cannot disinvest (shed unproductive customer capital), something that never happens with physical capital. This asymmetry arises because deposit inflows, unlike the acquisition of new machines, are not under the bank’s control, and can force costly financial adjustments such as costly equity issuance.

We also analyze how bank lending responds when its capitalization deteriorates. When k is high, the bank funds additional lending through wholesale borrowing—short-term debt that it can freely adjust. As k declines, the bank deleverages by retiring this wholesale funding first, since it is the controllable part of the liability structure. When k approaches the danger zone, the bank goes further: it shifts from issuing bonds to holding safe assets. Having lost the ability to reduce risk on the liability side (because deposits cannot be shed), the bank reduces risk on the asset side instead. This substitution from risky lending toward safe-asset holdings represents a new channel that connects a bank’s equity capital to its lending policy.

This mechanism explains why banks may cut lending in response to deposit inflows—a puzzle that confounded many observers during the pandemic. When deposits flood in without a corresponding increase in equity, k falls and leverage rises, bringing the bank closer to breaching the leverage requirement and to costly equity issuance. The bank endogenously becomes more risk-averse and pulls back on lending, because loans carry the risk of losses that could further erode capital. Far from fueling a credit boom, deposit inflows can trigger a credit contraction.

Our analysis yields a striking insight into leverage regulation. In 2020, regulators relaxed the SLR to help banks absorb deposit inflows. This had the intended short-run effect: it raised the deposit q, reduced the probability of costly equity issuance, and stimulated both deposit-taking and lending. But the long-run effect runs in the opposite direction. When leverage constraints are tight, banks must issue equity more frequently. To compensate shareholders for these recurring costs of equity issuance, banks reach for yield by loading up on risk. Relaxing the SLR eliminates this motive, making banks happy to hold safer assets over the long run. Conversely, tighter leverage requirements—while curbing risk-taking and lending in the short term—can induce more aggressive risk-taking over the long run. Currently, the discussion around bank leverage regulation has again become a hotly debated issue. One source of differences of opinion around the SLR for regulators is the time horizon when assessing the impact of leverage rules; those with a short horizon draw different conclusions from those with a longer perspective.

Low interest rates compound the problem. A bank manages deposits primarily through the deposit rate: raise it to attract more deposits, lower it to discourage inflows. The gap between the prevailing market rate and the zero lower bound determines how much headroom the bank has. When market rates are high, the bank can offer a generous deposit rate in good times and still have space to cut the deposit rate should capital run thin. When market rates are near zero, the bank starts with almost no headroom. The deposit rate is then already at the floor even for a well-capitalized bank, and the bank cannot push deposits away by lowering the rate when it becomes under-capitalized and needs to deleverage. Low rates therefore do not just squeeze margins—they strip banks of their primary tool for managing leverage risk. This provides a new channel that helps explain why low interest rates can impair monetary policy transmission: banks, unable to manage deposit-flow risk, become more conservative in lending even as policymakers try to stimulate credit supply.

In sum, deposits have long been considered a bank’s cheap source of funding—but they can become a burden when a bank’s capital cushion gets too thin. A flood of deposits can push leverage against regulatory limits, force expensive equity issuances, and cause the bank to pull back on lending rather than expand it to preserve regulatory slack. This is exactly what played out during the Covid-19 pandemic. A bank’s ability to manage deposits depends on its room to adjust deposit rates, and such ability evaporates when the market rates are near zero and deposit rates cannot be further reduced to turn away unwanted deposits. While regulators can offer relief by loosening leverage rules, doing so distorts banks’ risk-taking behavior with different short- and long-run effects.